Sources over slogans

When we describe a fee pattern or funding rail, we tie it to how the product category usually behaves—so you know what to verify in live disclosures.

CLS Money Y LLC

Tell us what you need and where you live; we narrow cash-flow advances, personal installment loans, and higher-cost credit to partners whose own published rules line up with that snapshot. Along the way, CLS Money publishes reviews and long reads so fee paths and disclosure language are easier to sanity-check before you leave for a lender’s site.

ReviewsArticlesAboutContactiOS app

If you continue with a partner we list, that company may compensate us; it does not raise the price you would have seen going to them directly.

Partners we review & match

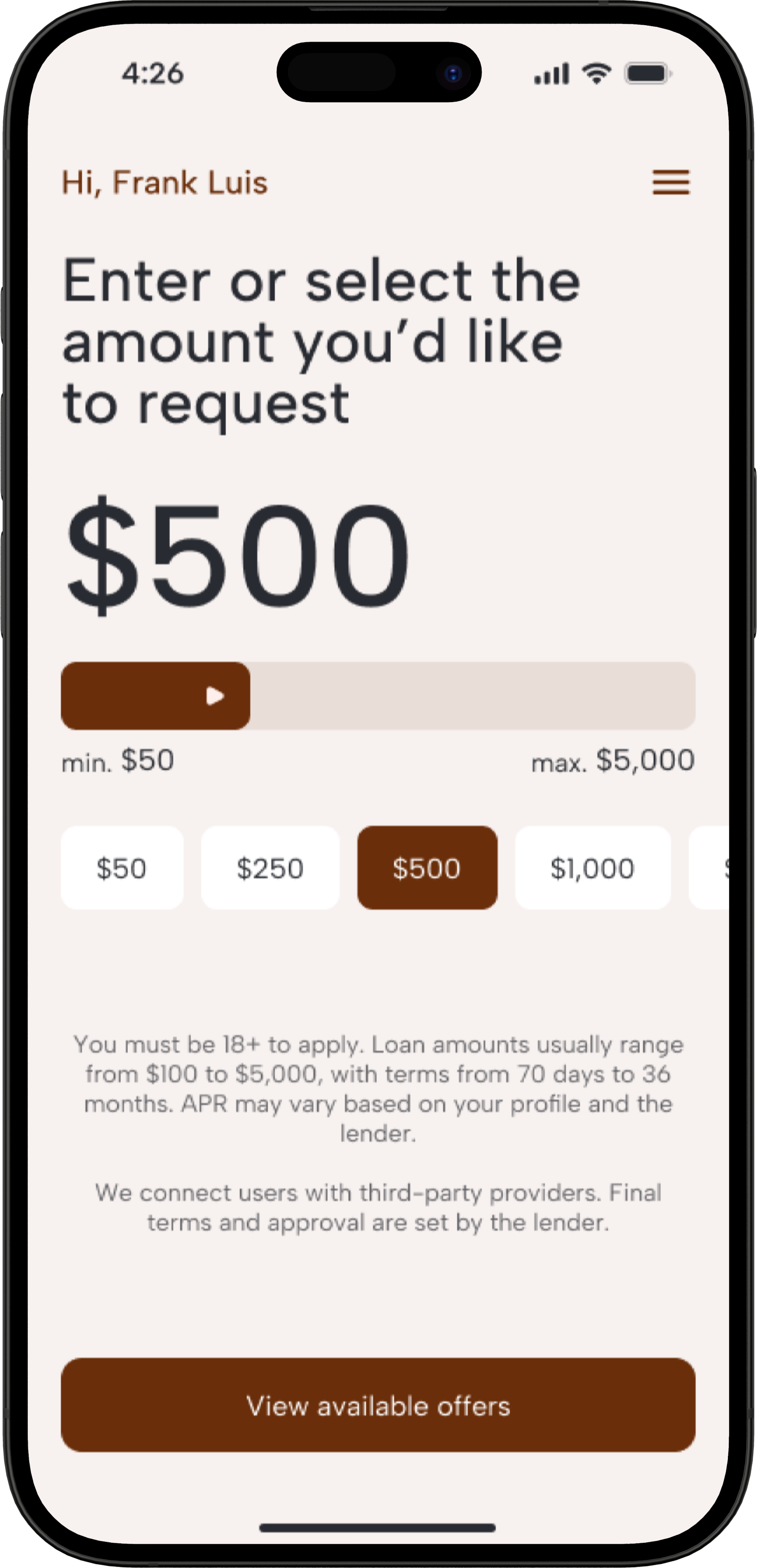

You must be 18+ to apply. Loan amounts are typically up to $1,000, with terms from 70 days to 36 months. 5.99% to 35.99% APR may vary based on your profile and the lender.

We connect users with third-party providers. Final terms and approval are set by the lender.

Full loan rates & lane breakdownCLS Money Y LLC is organized in Colorado with a published mailing address on every page—no anonymous “compare” shell.

Tables use published ranges from lender sites and help centers—not invented “typical” APRs or star ratings from thin air.

We earn fees when you move forward with some partners; we say so up front. That does not change the partner’s own pricing.

Privacy, app privacy, terms, California choices, and other notices—written for humans, not fine-print traps.

CLS Money Y LLC answers editorial and site questions by mail—see our contact page or write to [email protected]. We do not handle loan applications; providers set eligibility and offers on their own sites.

Trust here is structure: clear disclosures, visible address, and writing that admits tradeoffs instead of shouting urgency.

When we describe a fee pattern or funding rail, we tie it to how the product category usually behaves—so you know what to verify in live disclosures.

Tables help you shortlist; articles walk through APR mechanics, inquiries, and funding timing when you want the full picture.

Partner relationships may earn us fees when you engage. That does not change the price you pay the provider for the same offer.

Privacy (site and app), terms, financial-privacy notices, e-sign consent, and state opt-out pages live under Policies in the footer—same language whether you read on a laptop or phone.

Three steps. Nothing you pay us. Matching runs in the CLS Money iOS app today; this site is your editorial library.

How much you need, how soon, income type, and state—enough to filter partners by their published eligibility rules.

We surface cash-flow, personal loan, and higher-cost options whose own rules align with your profile. Ranking leans on eligibility overlap ahead of commercial incentives.

Read our write-up, then apply on the partner’s site. They set APR, approval, and funding—not CLS Money.

CLS Money for iPhone

Share amount, timing, income type, and state on your phone—see partners whose published rules may fit. This site is your editorial library; the app is where matching happens today.

These explain how we work and where numbers really live. They are educational—not legal or tax advice for your situation.

No. CLS Money Y LLC is a comparison and matching service. We do not make loans, set APR, or approve applications. Partners handle underwriting and funding after you choose to continue with them.

In the CLS Money iOS app. This website carries reviews, articles, and policies so you can research at your own pace before you install anything.

On the provider’s regulated disclosures —typically a Truth-in-Lending box for installment credit, plus any separate fee schedule for advance-style products.

We use neutral letter badges so you can scan quickly without implying a trademark partnership or paid logo placement.

We may receive compensation from partners when you choose to engage with them. That does not change what you pay the provider—and it does not determine match order.

We cannot. Approval, pricing, and limits are decided solely by the provider using your application and eligibility rules.

Confirm APR, finance charge, amount received, payment schedule, and optional fees match what you expected. If something moved, stop and ask support before you sign.

Published ranges from each provider’s site and help center—not your personal quote. Open a write-up for fees, eligibility, and what to verify before you apply.

Personal and higher-cost installment partners are on our reviews hub—with lane explainers for personal loans and higher-cost installment.

Longer explainers for when you want judgment, not jargon—pair them with our reviews hub when you are comparing live offers.

Cash-flow apps, personal loans, and higher-cost installment credit move money differently—here is how to match the product to the week you are having.

Open article

Soft pulls vs hard pulls—where each shows up, why pre-qualification is not an approval, and how to shop without bruising your file.

Open article

How filtering partners differs from lending, how we rank results, and how the app sits next to the site’s reviews.

Open articleWant more? Disclosures, funding timing, and other reads are in our articles library“click here to keep reading.